Visualizing Coronavirus’ “Winners”

Record breaking unemployment claims, sweeping shutdowns, and a volatile stock market have made predicting the full effect of COVID-19 near impossible. Yet what we can say with certainty is that the effects of this shock are strongly heterogenous. Nowhere is this clearer than in stock market returns.

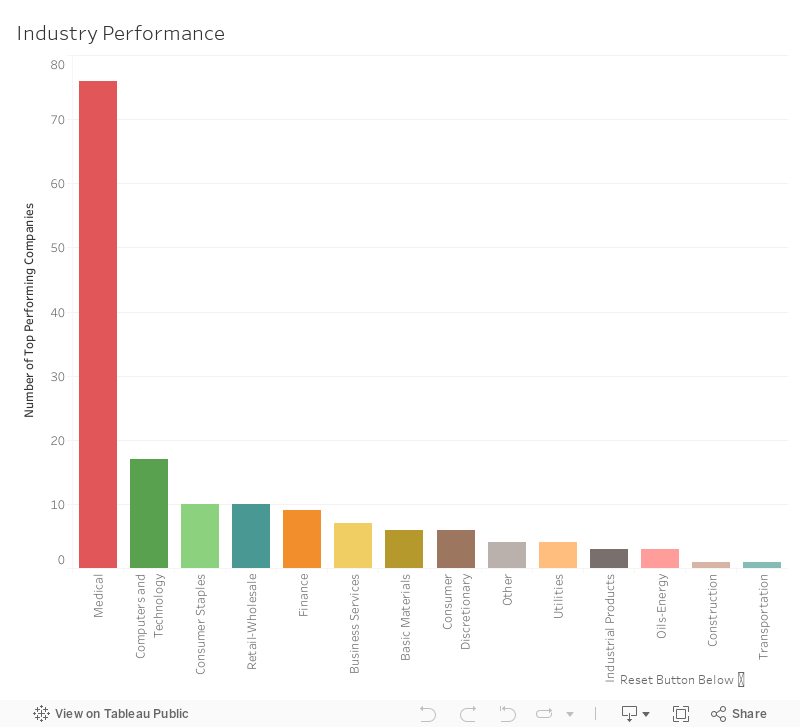

While the S&P 500 is down over 20% since mid-February and the Nasdaq Composite down 19%, some companies’ stock has soared more than tenfold. Of the highest performing stocks listed on U.S. exchanges, almost half are medical companies. Tech and finance companies follow in a distant second and third, with the trio accounting for two thirds of the top performers. To understand what is driving this outperformance we must examine the biggest success stories.

Fig 1: Medical companies make up 48 percent of top performing companies; tech and finance trail at 11 percent and 6 percent, respectively.

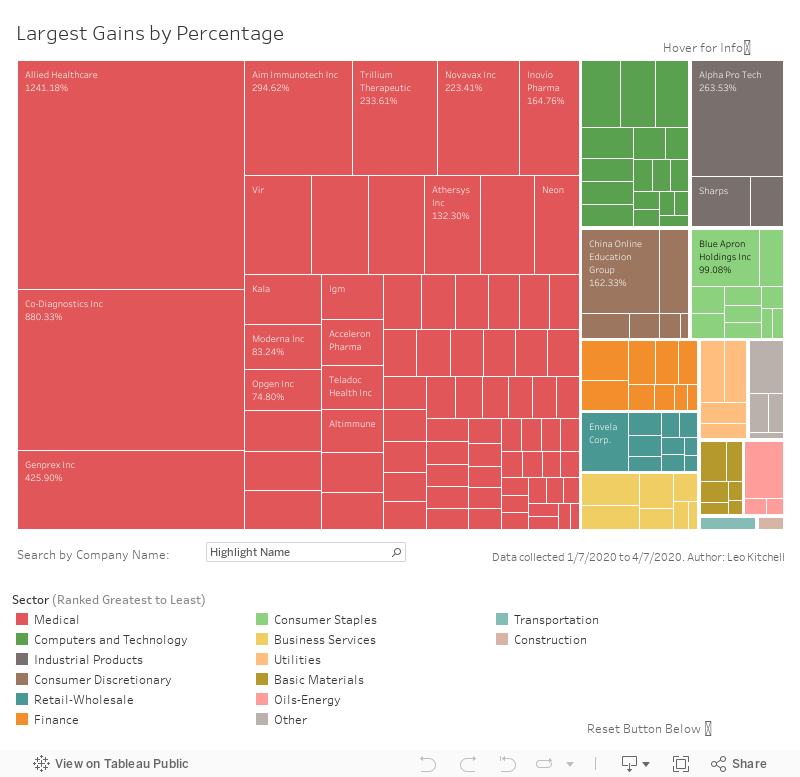

Allied Healthcare Products Inc, up more than 12 times its pre-virus value, has grown faster than any other company by far. The company manufactures emergency medical supplies, ventilators, and respiratory therapy equipment which are in critical demand as COVID-19 is a respiratory disease. In similarly short supply are testing kits, which explains Co-Diagnostics meteoric rise. The company provides low-cost molecular testing kits which can test both if a patient currently has the disease or has contracted the disease before.

Besides some exceptions which are developing novel cancer treatments, the remaining healthcare growth companies are largely focused on the Coronavirus. Aim Immunotech, Inovio, Moderna, Novavax, Athersys, Vir, and Bellerophon are just some of the many companies designing new treatments and testing whether existing drugs can be repurposed to fight COVID-19.

COVID-19’s influence also reaches upstream in the supply chain to industrial products stocks. Alpha Pro Tech, who produces disposable protective apparel has seen their share price more than triple. Lakeland Industries, one of Alpha Pro’s competitors, also grew at a record pace. Of course, these disposable clothes and masks cannot simply be thrown in the dump after use. Instead, a specialized medical waste disposal service like Sharps Compliance, up 75%, must be contracted.

Fig 2: Many small medical companies have seen rapid growth. In other sectors, returns are driven by just a handful of companies.

With approximately 95% of the U.S. and much of the rest of the world under stay at home orders, everything from work, to education, to leisure has been upended, but some are prospering. China Online Education Group, which teaches virtual English lessons in China and the Philippines, has grown 162% as quarantined citizens and students put their free time to productive use. To the chagrin of parents everywhere, these pupils may also be pursuing less productive ends; videogame studio Liquid Media is up 30%.

Balancing out this leisure is a significant growth in enterprise solutions for telecommuting. Zoom Telecommunications, up 58% even after a recent sell-off, has been a growth leader in this area as has Ringcentral, up 12%. However, replicating the modern day office at home requires more than just a video chat. Citrix systems, which provides IT, networking, and cybersecurity services has seen demand for their products increase as companies move to establish and secure their telecommuting networks. Cloud based tech companies like Zscaler and Cloudflare have both risen 29%, as companies look to give employees secure virtual access to corporate databases. To handle this increased bandwidth demand from both enterprise and consumer demand, companies have looked to providers like 21 Vianet, up 54%, which houses data centers and is the exclusive operator of Microsoft Azure and Office in China.

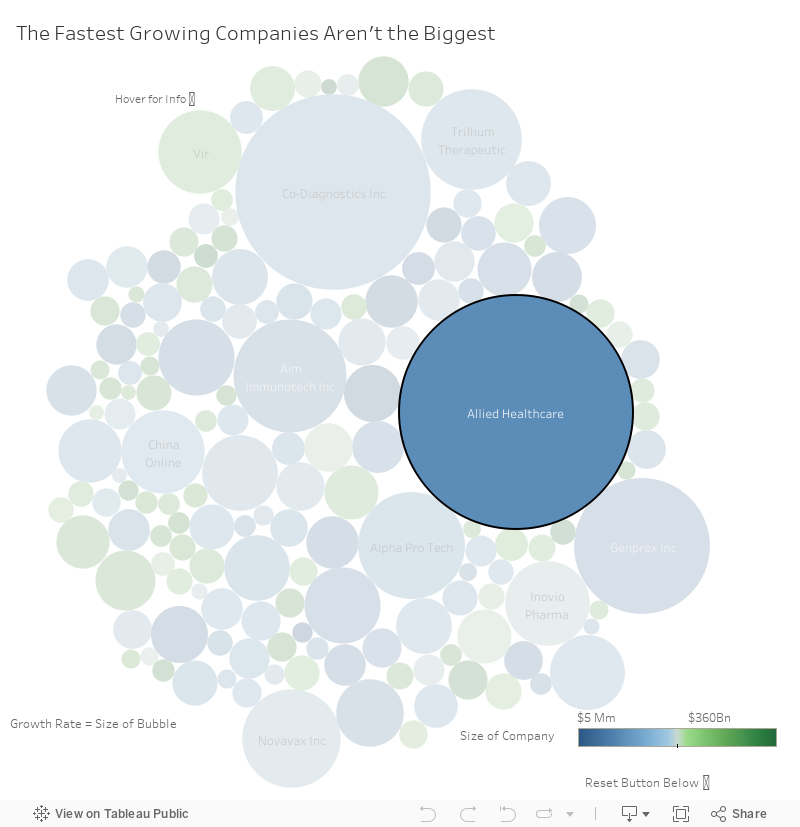

Fig 3: The fastest growing companies have been small companies with specialized products in high demand.

While the companies listed above were growing rapidly, not all were making significant contributions to the overall market. Large cap stocks are already too large to grow 1200% over three months, like Allied Healthcare did. Above, the color of the circle represents the market capitalization of the company with dark blue being the smallest, dark green the largest, and light blue-green in the middle. When measuring growth by the dollar amount added to the company’s total value, healthcare begins to dominate less as the small market cap of highly volatile pharmaceutical producers dampens extreme growth rates.

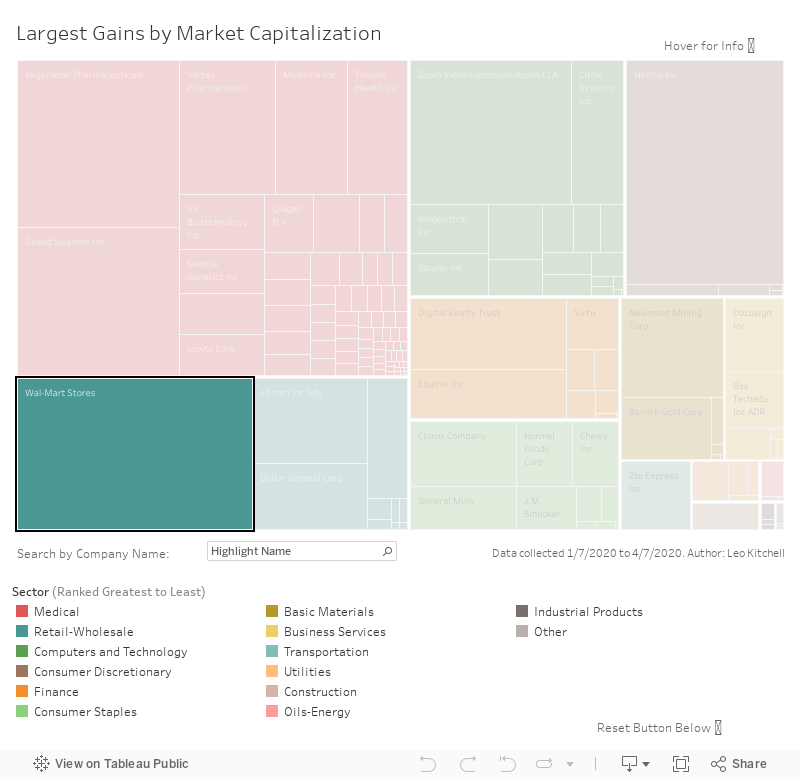

Fig 4: Even when weighting companies by their relative sizes, total returns are dominated by mid-cap and smaller large-cap companies. Behemoths like Amazon, while performing better than the market average, remain at valuations below pre-virus levels; Wal-Mart is one notable exception to this trend.

After adjusting for these differing market caps, wholesalers and consumer staple companies perform significantly better. Wal-Mart, Dollar General, and Grocery Outlet stores, up 6%, 11%, and 17%, have been packed with consumers stocking up on food and essentials. Notably, each brand prides itself on low prices, which have become increasingly salient as Americans are filing for unemployment at record pace.

Inside these stores, the newly price-conscious consumers are purchasing non-perishable goods like SPAM, trademark owned by Hormel Foods (up 8%) and Cheerios, owned by General Mills (also up 8%). Pet company Chewy Inc, up 14%, has also seen increased demand, albeit among those with less discerning palates.

There has even been growth in stocks that are hardly stocks at all. Precious metals are often considered a safe haven for investors in times of global turmoil. High demand for gold has driven Newmont Mining Corp stock up 16% on account of its reserves, which are the largest in the industry according to the company. Such reserves are not limited to mining companies. Envela Corp, which retails fine jewelry, has experienced a 69% increase in company value, driven by its large holdings of gemstones and bouillon.

So, where does all this information leave us? For investors, it’s a reminder that even among aggregate shocks there will always be opportunities to find returns. It may also mark a reversal of the last decade’s trend of index funds outperforming active managers. But the effects are more tangible than just some life lessons.

To understand the long term economic impacts of the COVID-19 crisis, we must return to the greater economic context. As we speak, small and medium sized businesses are running out of cash reserves and reaching the end of their lines of credit en masse. With the majority of the country likely to remain at home with no clear end in sight, many of these smaller businesses will go bankrupt in the coming weeks. It is in the post recession environment that we must consider our current success stories.

With local competition reduced, the financially fittest companies will be well positioned to merge or acquire distressed companies in complementary business segments. Alternately, successful businesses could opt for organic growth, investing internally with their excess cash while the rest of the market gets back on its feet. This head start in investment would provide a competitive edge and likely spur further growth. While the coming months will bring new uncertainties and swings in fortune, the largest boxes shown above may well turn out to be the largest success stories of the post COVID-19 recovery, too.

Article written and researched by Leo Kitchell.